Note: if images don't appear please enable "display / load images" in your email program. |

|

|

|

Issue: 481

February 3, 2025 |

|

|---|

|

|

“If everything is important, then nothing is.” |

|

|

|

|---|

|

|

Greetings,

Welcome to this week's Advisor Training newsletter. Our goal is to provide training, education and insights for those who adhere to our counter-cultural and sometimes counter-intuitive investment and business philosophy. |

|

|---|

|

|

-

Main event: Updated 9 Facts of the Market.

-

Review of Nick's February Advisor Newsletter.

-

Brief overview of Jackson VA Income Riders

-

17 Tips that Guarantee Success #12: AF MasterMind Telegram chatroom.

-

Brief summary of Epiphany #5: Prompt, Clear, Two-Way Communication.

-

Review of last week's quiz.

-

Updates, News and Announcements.

|

|

|---|

|

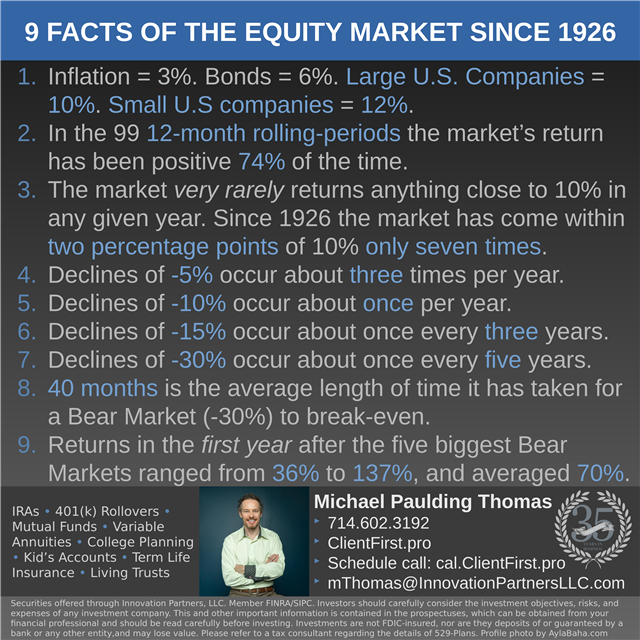

These are the updated 9 stats of the market as discussed at MKOM. |

|

|---|

|

|

|

Prologue from Nick...

The lead essay in this issue is my personal saga of rebalancing, an event that occurred as it always does on the first trading day of the year. This year, it inevitably involved the jettisoning of a fair amount of big tech exposure. A matter of days after the drafting of this essay, that bluest of all blue chip tech stocks, Nvidia, went down 17% in a day, mousetrapping a whole generation of performance-chasers and wiping out $589 billion of stock market value, a new world record.

“Sometimes,” as my gimlet-eyed Sicilian-American wife always says, “God lets you watch.”

Also in this issue: an admittedly somewhat cranky rant about the rise and rise of (and I quote) “alternative investments,” a trend which I have difficulty seeing as salutary. Client’s Corner suggests a practical redefinition of investing versus speculating. And we update The 62-Year Scorecard, which remains for me the single most powerful statistical arrow in the quiver of the Behavioral Investment Counselor.

|

|

|---|

|

"I'm I was rummaging around in my notes and found the contact info for a pretty good prospect I had forgotten about. Thing is, he's cousins with my ex-boyfriend. Should I toss it out or pursue?" |

|

|---|

|

Go for it! Your ex-boyfriend is probably happily married now anyway.

- Contact the ex-boyfriend's cousin over LinkedIn.

- Don't mention the ex-boyfriend. Just pretend he doesn't exist.

- Simply ask the cousin this question:

"Jerry, hope you are well. I'm writing a quarterly newsletter on problems that people tend to have with their money. Anything stumping you related to your GE pension plan or Social Security

payouts? I'm happy to write about it in the next edition."

- The cousin may not want to do business with you because of your past...

- However, that's no reason to construct imaginary barriers that don't exist.

- He may be a great referral source.

- He may have a company seminar where he needs a financial speaker.

- He may have a neighbor with a 401(k) rollover he has no clue about.

- He may appreciate your newsletter and send it to a friend.

Unless you really messed up with your ex-boyfriend, causing everyone in their family to hate you, give it a try. Chances are they trust you more than the random advisor cold calling them to sell whole life, and may be willing to engage in a positive way.

Just provide outstanding value to people and let them decide; don't destroy opportunities because of how you think people may feel about you. |

|

|---|

|

As quickly as possible, get to:

- 50 securities accounts.

- $50,000 income.

- $50,000 annual recurring revenue (ARR).

Until you do, don't over-analyze the business, just DO. |

|

|---|

|

Stop Acting Rich by Thomas Stanley

How the less affluent have fallen into the elite luxury brand trap that keeps them from acquiring wealth and details how to get out of it by emulating the working rich as opposed to the super elite. |

|

|

|

|

“Independent agents aren’t tied to one company, so they can offer you more options, saving you time and money.” |

|

|

|

|---|

|

IP offers Broker/Dealer, Advisory and Insurance services and is not tied to any product sponsors, allowing us to freely choose the best investment solutions for each individual client. Note: our Group is primarily a equity-mutual fund and term insurance shop, but for some clients it is beneficial to have access to a variety of offerings.

Here is just a small sampling of what we have on offer: Equities, Fixed Income, ETF, Mutual Funds, 529 plans, Variable Annuities, Options. Managed Accounts, Lifetime Minimum Guarantee Income, High Net Worth insurance wraps, Opportunity Funds, Model Portfolios, Alternative Investments, Family Office, Hedge Funds, Managed Futures, Private Equity, REITs, LPs. Multi-Custodian RIA Platforms: Axos, Folio/Goldman Sachs, Schwab, Fidelity, BNY Mellon/Pershing, US Bank, and others. Private Placements, Life Insurance and Annuity Products. Investment Banking and Succession Planning Services. Asset Protection Trusts, Charitable Giving and Legal Services. Manage Bitcoin and Etherium for customers using Flourish. All types of life insurance and annuities from dozens of providers. Accident insurance, Health Insurance, Disability insurance, Auto insurance via a referral program, Mortgage referral program. Living Trusts, Land Trusts, LLCs. And much, much more. |

|

|---|

|

Which one of the following is NOT a benefit of a Roth IRA? |

|

|---|

|

-

Withdrawals not subject to taxes.

-

Contributions are tax deductible.

-

No required minimum distributions.

|

|

|---|

|

Answer = 2

- Qualified withdrawals from a Roth IRA are generally tax-free.

- Contributions to a Roth IRA are made with after-tax dollars, hence they are not tax-deductible. This is unlike traditional IRAs where contributions might be deductible.

- Roth IRAs do not require you to take minimum distributions during the lifetime of the original owner, providing more flexibility in retirement planning."

|

|

|---|

|

Michael Paulding Thomas

Securities Principal & Advisor Development

Over three decades of training part-time and full-time financial advisors. Developed 2 $200k-earners, 10 $100k-earners, 15 part-time $50k-earners and built a $1.6M revenue sales force.

|

|

|

|

|

|

| |

|

|