Note: if images don't appear please enable "display / load images" in your email program. |

|

|---|

|

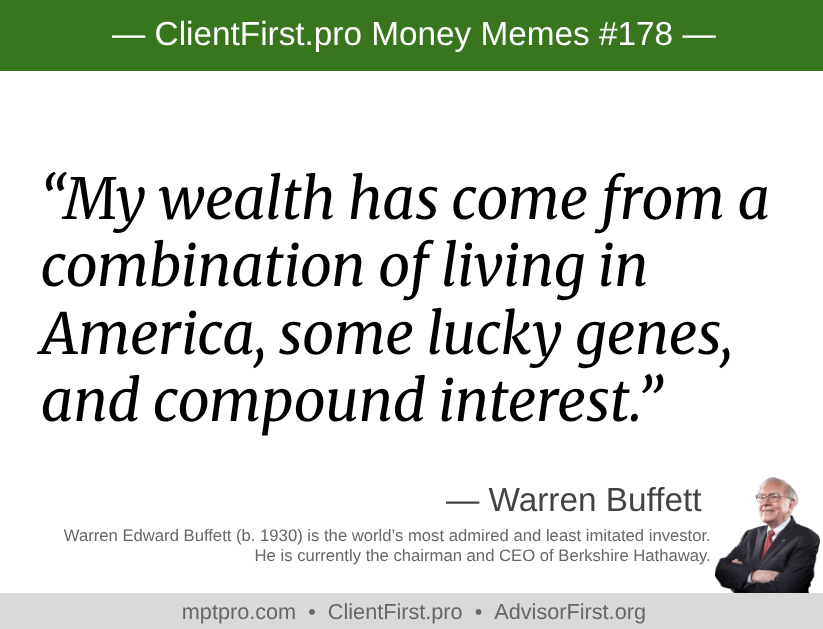

“The individual investor should act consistently as an investor and not as a speculator.” |

|

|

|

|---|

|

|

|

I was thrilled to receive wonderful kudos (on LinkedIn) from one of my clients, and I wanted to share! Thank you for the kind words Sergei!

|

|

|---|

|

|

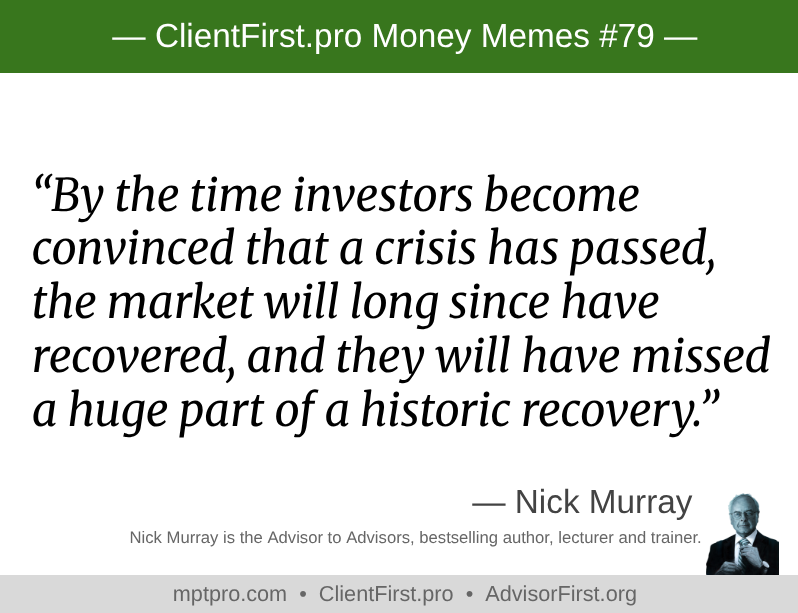

In a rare occurrence Nick Murray didn't publish a Client's Corner this month (he'll be back next month). So, I decided to present you the issue from August 2009. The content is very relevant to today, as all fundamental principles are. Remember, This Time

ISN'T Different. |

|

|---|

|

MICHAEL'S TRAINING OF THE MONTH |

|

|---|

|

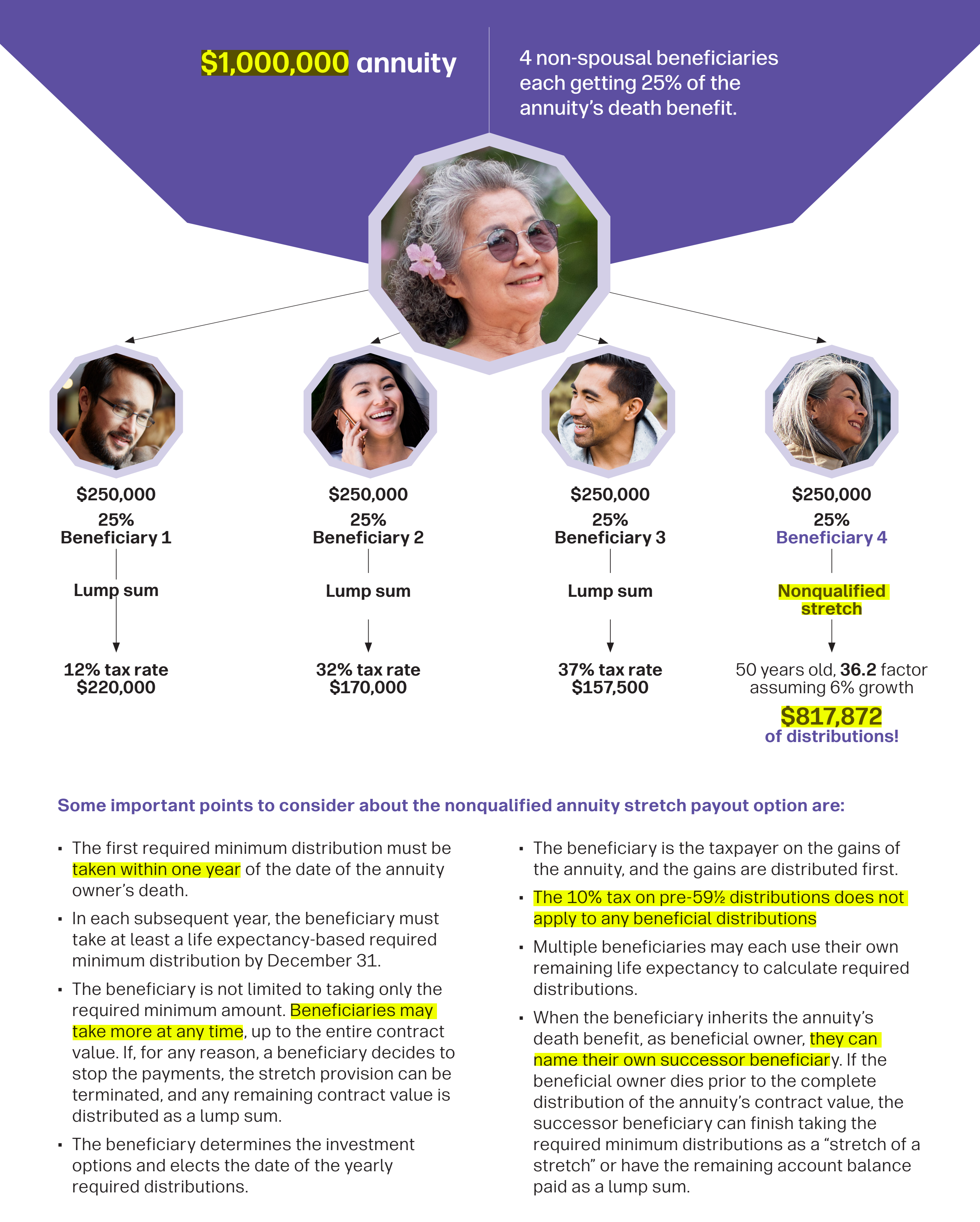

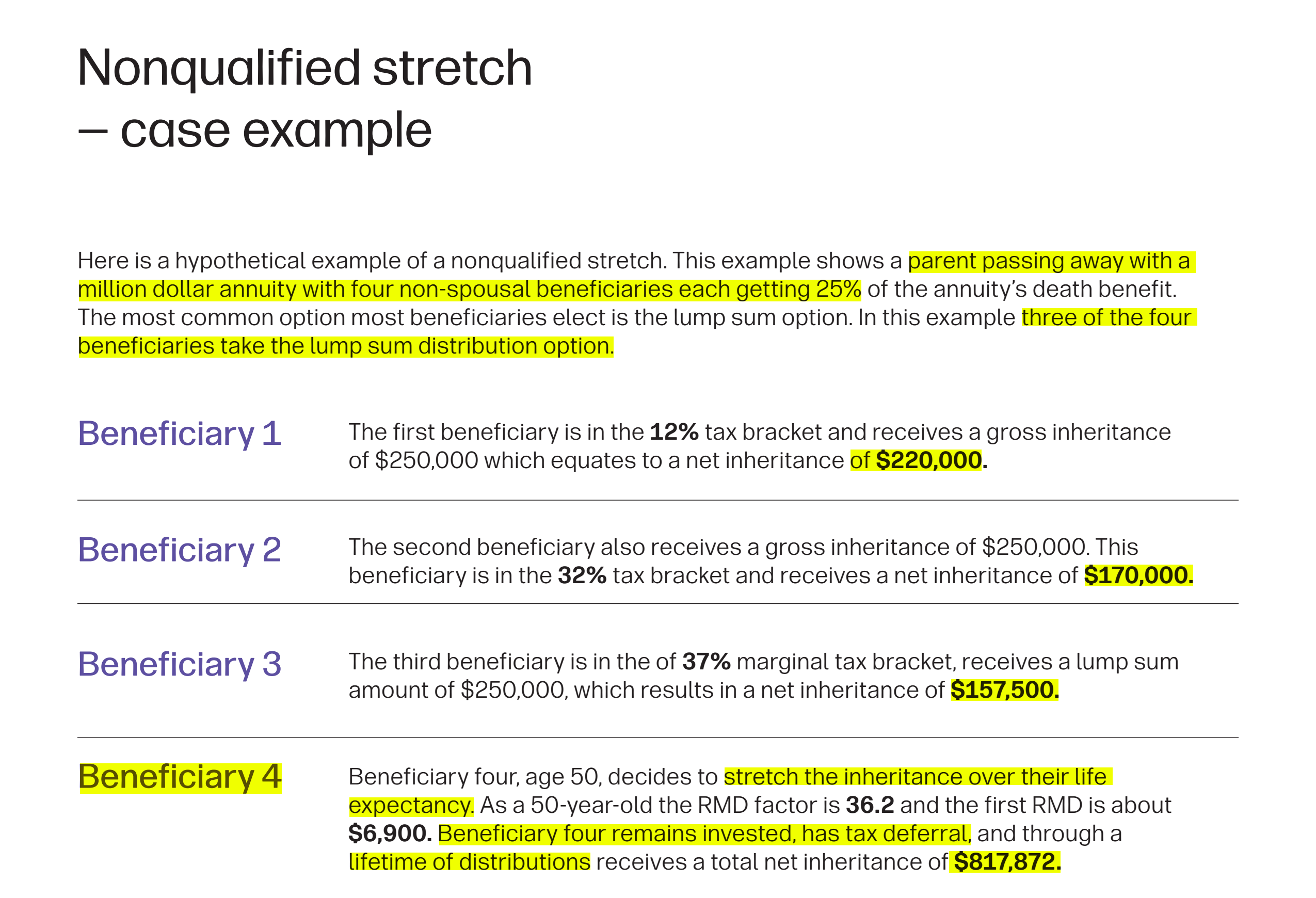

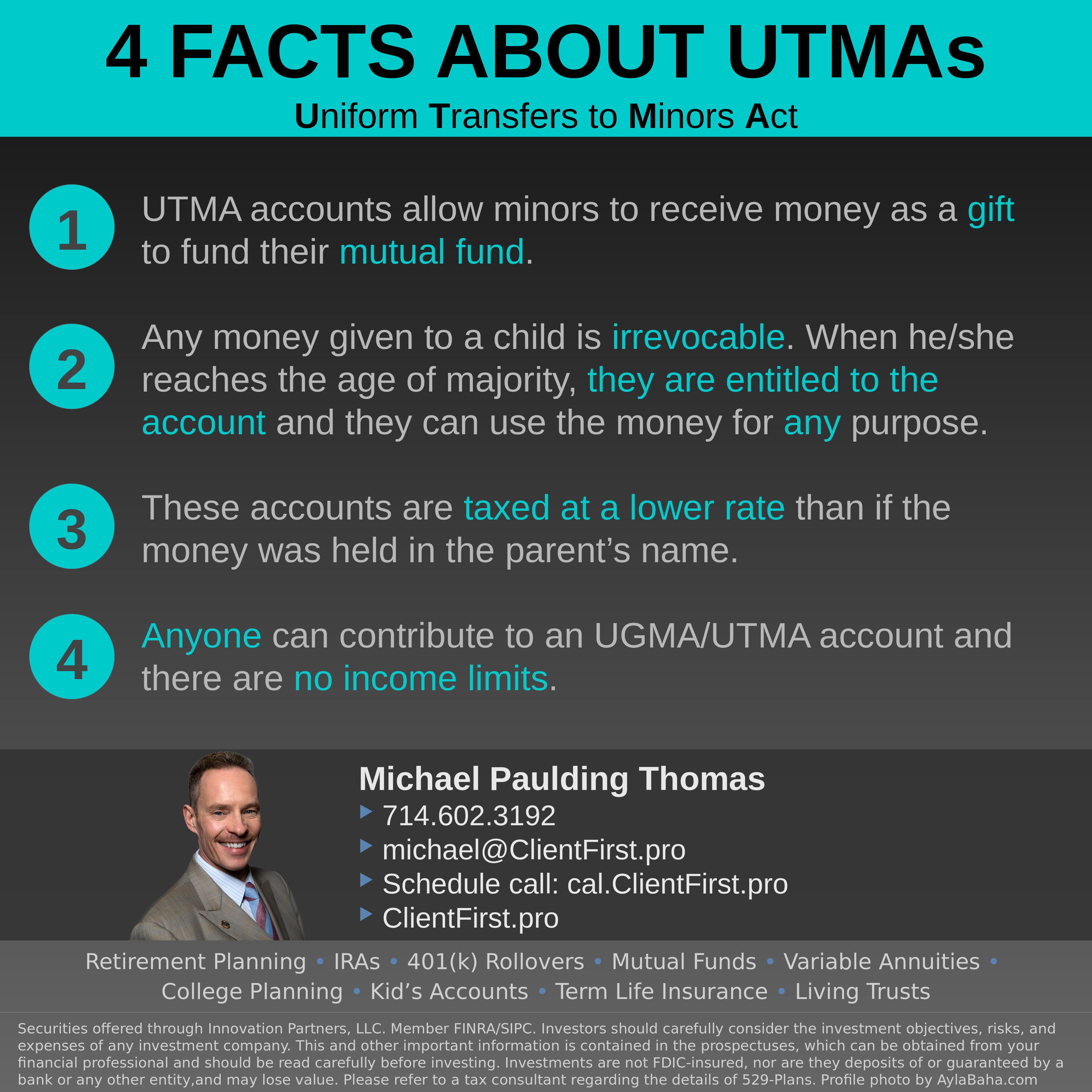

Variable Annuity: Non-Qualified Beneficiary Stretch |

|

|---|

|

Variable annuities (which is just a wrapper around equity mutual funds - we always use American Funds) offers many benefits. One of which is the ability to create a tax-reduced transfer of assets to your beneficiaries, called a "stretch". This is seen in the fourth person in the above example. |

|

|---|

|

|

2025 Retirement Limits

Roth Max Income Limits

⯎ Single: $150,000

⯎ Joint: $236,000

IRA/Roth Contribution Limits

⯎ Age <50: $7,000

⯎ Over 50+: $8,000 |

|

|

401k Contribution Limits

⯎ Age <50: $23,500

⯎ Age: 50-59: $31,000

⯎ Age 60-63: $34,750

SEP IRA Contribution Limit

⯎ 25% of employee's compensation, or $70,000, whichever is less |

|

|---|

|

|

The Case for Dividend Growth: Investing in a Post-Crisis World

by David Bahnsen

Nick Murray says:

"I think so highly of this book — and David — that I’ve bent my unbreakable rule never to provide jacket blurbs. The compounding of growing dividends is at the core of David’s investment policy. You will particularly wish to consider his recommended withdrawal strategy, which I’ve not seen anywhere else."

|

|

|

|

|

Don't overlearn lessons: Staying nimble in turbulent markets |

|

|---|

|

Youtube - July 30, 2025 - 31 minutes |

|

|---|

|

“When the thesis changes, you have to change with it,” says portfolio manager Julian Abdey. From earning the nickname Dr. Doom as a bank analyst in the leadup to the global financial crisis to scenario planning throughout the pandemic, Julian has honed the skill of doing his own research to gain an edge and stay ahead of change by embracing it. He sits down with Mike Gitlin to discuss how he gains conviction, where he sees potential “oaks” among small-cap “acorns,” and how his brief foray into life as an academic economist influences his approach to risk management. |

|

|---|

|

Is the trade war killing globalization? |

|

|---|

|

The U.S.-led trade war may change globalization in a profound way, but it won’t kill it, says Capital Group portfolio manager Steve Watson, a global equity investor with 37 years of experience. “Globalization isn’t dead,” he insists. |

|

|---|

|

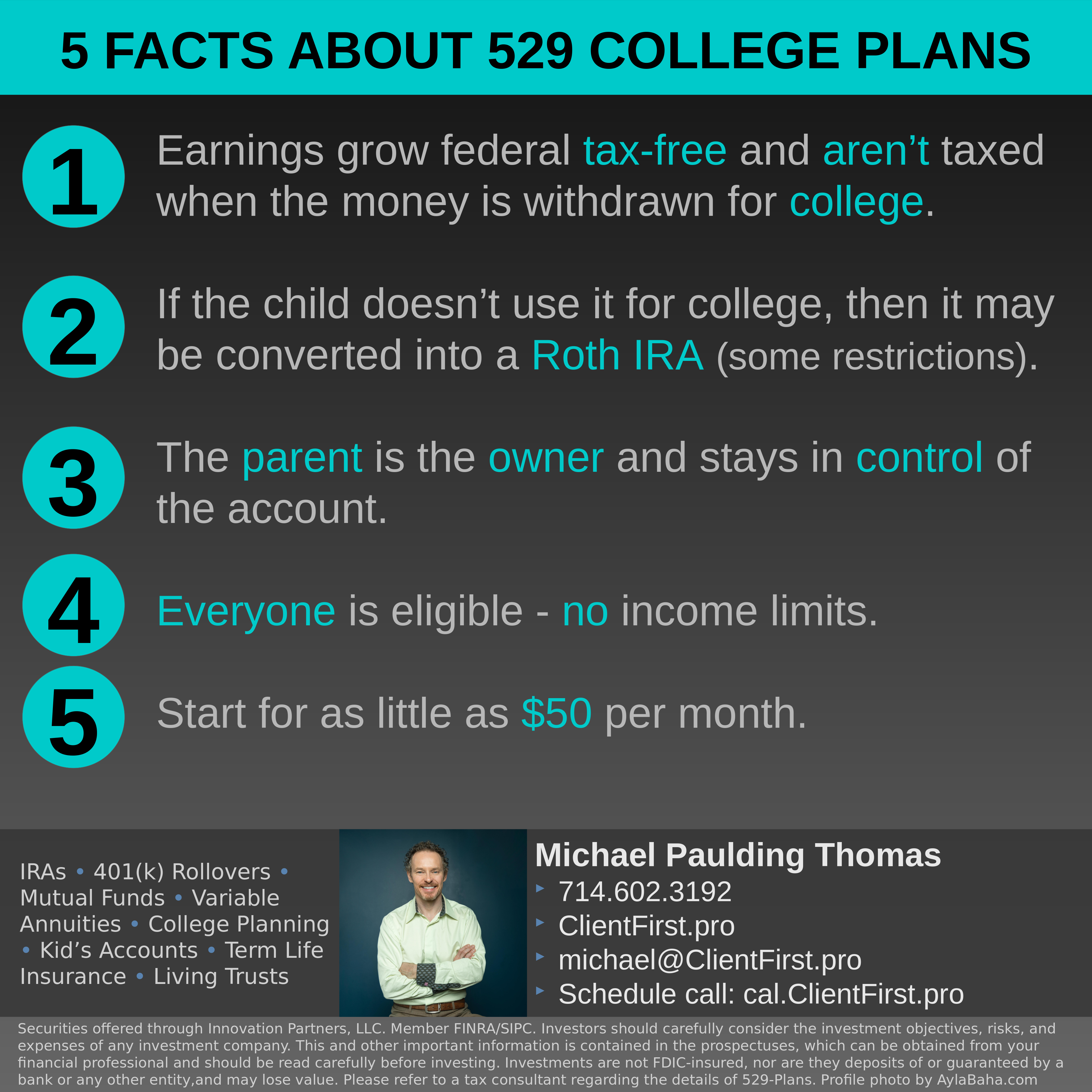

Grandparents want to set-up 529-plans for their four grandchildren. What is the maximum they can contribute in one year (2025) without making it a taxable gift? |

|

|---|

|

- $160,000

- $320,000

- $480,000

- $760,000

- $1,280,000

- No limit

|

|

|---|

|

Answer = #3. $760,000

In 2025, the annual gift tax exclusion is $19,000 per recipient for an individual donor, or $38,000 per recipient for a married couple filing jointly who elect to split gifts. Since the grandparents are setting up 529 plans for their four grandchildren, they can take advantage of this exclusion for each grandchild. Additionally, 529 plans offer a unique option called 5-year gift-tax averaging, which allows them to front-load up to five years' worth of gifts in a single year without incurring gift tax, as long as they don’t make additional gifts to the same beneficiary during the next four years.

Here’s how it works for the grandparents in 2025:

- As a married couple, they can contribute up to $38,000 per grandchild in a single year without it being a taxable gift. For four grandchildren, this would be:

- $38,000 × 4 = $152,000 total

- With 5-year gift-tax averaging, they can contribute up to five times the annual exclusion amount per grandchild in one lump sum, treated as if spread evenly over five years. For 2025, this means:

- $19,000 × 5 = $95,000 per grandchild per grandparent.

- Since they’re a married couple, they can double this to $190,000 per grandchild ($95,000 from each spouse).

- For four grandchildren, this would be: $190,000 × 4 =$760,000 total

Thus, the maximum the grandparents can contribute in 2025 to the four 529 plans without making it a taxable gift is $760,000, provided they elect the 5-year averaging option and file IRS Form 709 to report it. This assumes they make no other gifts to these grandchildren over the next four years. If they prefer to contribute annually without the 5-year election, the maximum would be $152,000 for 2025. They should consult a tax advisor to confirm their specific situation and ensure compliance with IRS rules.

|

|

|---|

|

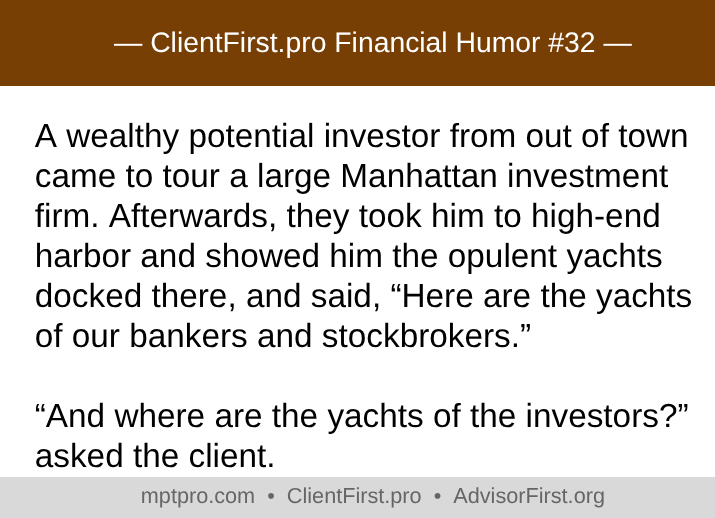

MONEY MEMES AND A LITTLE HUMOR |

|

|---|

|

With over 36 years in the industry, I’ve cultivated a broad network of professionals. If you need guidance on estate planning, taxes, bookkeeping, mortgages, real estate, reverse mortgages, notary services, health or car insurance, or even traffic violations, I'd be happy to introduce you to an expert.

|

|

Michael Paulding Thomas

Financial Advisor, Registered Representative, Securities Principal. Series 6, 26, 63, 65, Life

Since 1989 I’ve been helping families make smart choices about building a guaranteed income during retirement.

|

|

|

|

|

Retirement Planning • IRAs • 401k's • Rollovers • Mutual Funds • Variable Annuities • College Planning • Term Life Insurance • Living Trusts |

|

|---|

|

|

| |

|

|